Notes to the Financial Statements

-

1. General Information

CITIC Limited (the “Company”) was incorporated in Hong Kong and formerly known as CITIC Pacific Limited (“Former CITIC Pacific”), the shares of which are listed on the Main Board of the Stock Exchange of Hong Kong Limited. The address of its registered office is 32nd Floor, CITIC Tower, 1 Tim Mei Avenue, Central Hong Kong. Before 8 May 2014, the former CITIC Limited (“Former CITIC Limited”) held 57.51% equity interests in Former CITIC Pacific through its overseas wholly-owned subsidiaries, and the shareholders of Former CITIC Limited were CITIC Group Corporation (“CITIC Group”) and Beijing CITIC Enterprise Management Co., Ltd. (“CITIC Enterprise Management”), a wholly-owned subsidiary of CITIC Group.

In March 2014, a framework agreement to transfer the shares of Former CITIC Pacific was entered into between several parties. Pursuant to the framework agreement, the subsidiaries of Former CITIC Limited which held the shares of Former CITIC Pacific transferred these shares to certain overseas wholly-owned subsidiaries of CITIC Group (“the Transfer”). The Transfer was approved by the regulatory authorities and completed on 8 May 2014.

On 16 April 2014, CITIC Group, CITIC Enterprise Management and Former CITIC Pacific entered into a share transfer agreement, pursuant to which Former CITIC Pacific acquired 100% equity interests in Former CITIC Limited from CITIC Group and CITIC Enterprise Management (“the Acquisition”).

The Acquisition was completed on 25 August 2014. The name of Former CITIC Limited was changed from CITIC Limited to CITIC Corporation Limited (“CITIC Corporation”) and the name of Former CITIC Pacific was changed from CITIC Pacific Limited to CITIC Limited. Upon the completion of the Acquisition, CITIC Group held 77.9% equity interests in the Company through its overseas wholly-owned subsidiaries.

In 2015, CITIC Group disposed certain equity interests in the Company through its overseas wholly-owned subsidiaries, and the Company issued some new ordinary shares (Note 44(a)). As at 31 December 2015, the equity interests held by CITIC Group in the Company through its overseas wholly-owned subsidiaries decreased from 77.9% to 58.13%.

The Company and its subsidiaries (collectively referred to as the “Group”) are principally engaged in financial services, resources and energy, manufacturing, engineering contracting, real estate and other businesses.

The parent and the ultimate holding company of the Company is CITIC Group.

-

2. Significant accounting policies

(a) Basis of preparation

These financial statements have been prepared in accordance with all applicable Hong Kong Financial Reporting Standards (“HKFRS”), which in collective term includes all applicable individual Hong Kong Financial Rerpoting Standards, Hong Kong Accounting Standards (“HKAS”) and Interpretations issued by the Hong Kong Institute of Certified Public Accountants (“HKICPA”) and accounting principles generally accepted in Hong Kong. These financial statements also comply with the applicable disclosure provisions of the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited. A summary of the significant accounting policies adopted by the Group is set out below.

The HKICPA has issued a number of amendments to HKFRS that are first effective for the current accounting period of the Group. Impacts of the adoption of the amended HKFRS are discussed below:

(i) Amendments to HKAS 19, Defined benefit plans: Employee contributions

This narrow scope amendment applies to contributions from employees or third parties to defined benefit plans. The amendment distinguishes between contributions that are linked to service only in the period in which they arise and those linked to service in more than one period. The amendment allows contributions that are linked to service, and do not vary with the length of employee service, to be deducted from the cost of benefits earned in the period that the service is provided. Contributions that are linked to service, and vary according to the length of employee service, must be spread over the service period using the same attribution method that is applied to the benefits.

(ii) Annual improvements to HKFRS 2010-2012 cycle

Amendments to HKFRS 8, Operating segments

The standard is amended to require disclosure of the judgements made by management in aggregating operating segments and a reconciliation of segment assets to the entity’s assets when segment assets are reported.-

Amendments to HKAS 16, Property, plant and equipment and HKAS 38, Intangible assets

Both standards are amended to clarify how the gross carrying amount and the accumulated depreciation are treated where an entity uses the revaluation model. Amendments to HKAS 24, Related party disclosures

The reporting entity is not required to disclose the compensation paid by the management entity (as a related party) to the management entity’s employee or directors, but it is required to disclose the amounts charged to the reporting entity by the management entity for services provided.

(iii) Annual improvements to HKFRS 2011-2013 cycle

Amendments to HKFRS 3, Business combinations

It clarifies that HKFRS 3 does not apply to the accounting for the formation of any joint arrangement under HKFRS 11 in the financial statements of the joint arrangement.-

Amendments to HKFRS 13, Fair value measurement

It clarifies that the portfolio exception in HKFRS 13, which allows an entity to measure the fair value of a group of financial assets and financial liabilities on a net basis, applies to all contracts (including non-financial contracts) within the scope of HKAS 39 or HKFRS 9. Amendments to HKAS 40, Investment property

Preparers also need to refer to the guidance in HKFRS 3 to determine whether the acquisition of an investment property is a business combination.

The adoption of the above amendments has no material impact on the financial statements of the Group. The Group has not applied any new standard or interpretation that is not yet effective for the current accounting period.

In addition, the requirements of Part 9 “Accounts and Audit” of the new Hong Kong Companies Ordinance (Cap. 622) came into operation during the year. The Group has concluded that the impact is unlikely to be significant and will primarily only affect the presentation and disclosure of information in consolidated financial statements.

(b) Functional currency and presentation currency

The functional currency of the Company is Hong Kong dollars (“HK$”). The functional currencies of overseas subsidiaries are determined in accordance with the primary economic environment in which they operate, and are translated into HK$ for the preparation of the consolidated financial statements (see Note 2(h)). The financial statements of the Group are presented in HK$ and, unless otherwise stated, expressed in million of HK$.

(c) Basis of measurement

The measurement basis used in the preparation of the consolidated financial statements is the historical cost basis except that the following assets and liabilities are stated at their fair values as explained in the accounting policies set out below:

– investment properties (see Note 2(l));

– financial assets and liabilities at fair value through profit or loss (including trading financial assets or trading financial liabilities) (see Note 2(i));

– available-for-sale financial assets, except for those whose fair value cannot be measured reliably (see Note 2(i)); and

– fair value hedged items (see Note 2(j)(i)).

(d) Use of estimates and judgement

The preparation of these consolidated financial statements requires management to make judgements, estimates and assumptions that affect the application of policies and reported amounts of assets, liabilities, income and expenses. The estimates and associated assumptions are based on historical experience and various other factors that are believed to be reasonable under the circumstances, the results of which form the basis of making the judgements about carrying values of assets and liabilities that are not readily apparent from other sources. The estimates and underlying assumptions are reviewed on an ongoing basis. Actual results may differ from these estimates.

Judgements made by management that have significant effect on the financial statements and estimates with a significant risk of material adjustment in subsequent period are described in Note 3. Revisions to accounting estimates are recognised in the period which the estimates are revised and in any future periods affected.

(e) Subsidiaries and non-controlling interests

(i) Business combinations involving entities under common control

A business combination involving entities under common control is a business combination in which all of the combining entities are ultimately controlled by the same party or parties both before and after the business combination, and that control is not transitory. The assets acquired and liabilities assumed are measured based on their carrying amounts in the consolidated financial statements of the ultimate controlling party at the combination date. The difference between the carrying amount of the net assets acquired and the consideration paid for the combination (or the total face value of shares issued) is adjusted against the capital reserve. Any cost directly attributable to the combination is recognised in profit or loss when incurred. The combination date is the date on which one combining entity obtains control of other combining entities.

(ii) Business combinations not involving entities under common control

A business combination not involving entities under common control is a business combination in which all of the combining entities are not ultimately controlled by the same party or parties both before and after the business combination. Where (1) the aggregate of the acquisition date fair value of assets transferred (including the acquirer’s previously held equity interest in the acquiree), liabilities incurred or assumed, and equity securities issued by the acquirer, in exchange for control of the acquiree, exceeds (2) the acquirer’s interest in the acquisition date fair value of the acquiree’s identifiable net assets, the difference is recognised as goodwill. If (1) is less than (2), the difference is recognised in profit or loss for the current period. The costs of equity or debt securities as a part of the consideration for the acquisition are included in the carrying amounts of these equity or debt securities upon initial recognition. Other acquisition-related costs are expensed when incurred. Any difference between the fair value and the carrying amount of the assets transferred as consideration is recognised in profit or loss. The acquiree’s identifiable assets, liabilities and contingent liabilities, if the recognition criteria are met, are recognised by the Group at their acquisition date fair value. The acquisition date is the date on which the acquirer obtains control of the acquiree.

The Group recognises any non-controlling interest in the acquiree on an acquisition-by-acquisition basis. Non-controlling interests in the acquiree that are present ownership interests and entitle their holders to a proportionate share of the entity’s net assets in the event of liquidation are measured at either fair value or the present ownership interests’ proportionate share in the recognised amounts of the acquiree’s identifiable net assets. All other components of non-controlling interests are measured at their acquisition date fair value, unless another measurement basis is required by HKFRS.

For a business combination not involving entities under common control and achieved in stages, the Group remeasures its previously-held equity interest in the acquiree to its fair value at the acquisition date. The difference between the fair value and the carrying amount is recognised as investment income for the current period; the amount recognised in other comprehensive income relating to the previously-held equity interest in the acquiree are transferred to investment income in the period in which the acquisition occurs.

(iii) Consolidated financial statements

The scope of consolidated financial statements is based on control and the consolidated financial statements comprise the Company and its subsidiaries.

Subsidiaries are entities over which the Group has control. The Group controls an entity when it is exposed to, or has the rights to, variable returns from its involvement with the entity and has the ability to affect those returns through its power over the entity.

When assessing whether the Group has power, only substantive rights (held by the Group and other parties) are considered.

An investment in a subsidiary is consolidated into the consolidated financial statements of the Group from the date that control commences until the date that control ceases.

Where a subsidiary was acquired during the reporting period, through a business combination involving entities under common control, the financial statements of the subsidiary are included in the consolidated financial statements as if the combination had occurred at the date the ultimate controlling party first obtained control. Therefore the opening balances and the comparative figures of the consolidated financial statements are restated. In the preparation of the consolidated financial statements, the subsidiary’s assets, liabilities and results of operations are included in the consolidated balance sheet and the consolidated statement of comprehensive income, respectively, based on their carrying amounts, from the date that common control was established. Net profit earned by the acquiree prior to the date of acquisition is separately disclosed.

Where a subsidiary was acquired during the reporting period, through a business combination involving entities not under common control, the identifiable assets, liabilities and results of operations of the subsidiaries are consolidated into the consolidated financial statements from the date that control commences, based on the fair value of those identifiable assets and liabilities at the acquisition date.

Non-controlling interests are presented in the consolidated balance sheet within equity, separately from equity attributable to the ordinary shareholders of the Company. Non-controlling interests in the results of the Group are presented on the face of the consolidated statement of comprehensive income as an allocation of the total profit or loss and total comprehensive income for the year between non-controlling interests and the ordinary shareholders of the Company. Loans from holders of non-controlling interests and other contractual obligations towards these holders are presented as financial liabilities in the consolidated balance sheet in accordance with Note 2(i).

When the amount of loss for the current period attributable to the non-controlling interest of a subsidiary exceeds the non-controlling interest’s portion of the opening balance of shareholders’ equity of the subsidiary, the excess is allocated against the non-controlling interests.

When the accounting period or accounting policies of a subsidiary are different from those of the Group, the Group makes necessary adjustments to the financial statements of the subsidiary based on the Group’s own accounting period or accounting policies. Intra-group balances, transactions and cash flows, and any unrealised profit or loss arising from intra-group transactions, are eliminated in preparing the consolidated financial statements. Unrealised losses resulting from intra-group transactions are recognised fully in profit or loss when evidence of impairment of assets being provided.

Where the Group acquires a non-controlling interest from a subsidiary’s non-controlling shareholders or disposes of a portion of an interest in a subsidiary without a change in control, the difference between the amount by which the non-controlling interests are adjusted and the amount of the consideration paid or received is adjusted to the reserve (capital reserve) in the consolidated balance sheet. If the credit balance of reserve (capital reserve) is insufficient, any excess is adjusted to retained earnings.

When the Group loses control of a subsidiary, it is accounted for as a disposal of the entire interest in that subsidiary, with a resulting gain or loss being recognised in profit or loss, and the Group derecognises assets, liabilities, non-controlling interests and other related items in shareholders’ equity in relation to that subsidiary. Any interest retained in that former subsidiary at the date when control is lost is recognised at fair value and this amount is regarded as the fair value on initial recognition of a financial asset (see Note 2(i)) or, when appropriate, the cost on initial recognition of an investment in an associate or joint venture (see Note 2(f)).

(iv) Investment in subsidiaries

In the Company’s balance sheet, an investment in a subsidiary is stated at cost less impairment losses (see Note 2(t)(ii)).

The results of subsidiaries are accounted for by the Company on the basis of dividends received and receivable.

(f) Associates and joint ventures

An associate is an entity in which the Group has significant influence, but not control or joint control, over its management, including participation in the financial and operating policy decisions.

A joint venture is an arrangement whereby the Group and other parties contractually agree to share control of the arrangement, and have rights to the net assets of the arrangement.

An investment in an associate or a joint venture is accounted for in the consolidated financial statements of the Group under the equity method. Under the equity method, the investment is initially recorded at cost, adjusted for any excess of the Group’s share of the acquisition-date fair values of the investee’s identifiable net assets over the cost of the investment (if any). Thereafter, the investment is adjusted for the post acquisition change in the Group’s share of the investee’s net assets and any impairment loss relating to the investment (see Note 2(t)(ii)). Any acquisition-date excess of the Group’s share of the fair value of the investee’s identifiable net assets over cost, the Group’s share of the post-acquisition, post-tax results of the investees and any impairment losses for the year are recognised in profit or loss, whereas the Group’s share of the post-acquisition, post-tax items of the investees’ other comprehensive income is recognised in other comprehensive income of the Group. The Group’s interest in associate or joint venture is included in the consolidated financial statements from the date that significant influence or joint control commences until the date that significant influence or joint control ends.

When the Group’s share of losses exceeds its interest in the associate or the joint venture, the Group’s interest is reduced to nil and recognition of further losses is discontinued except to the extent that the Group has incurred legal or constructive obligations or made payments on behalf of the investee. For this purpose, the Group’s interest is the carrying amount of the investment under the equity method together with the Group’s long-term interests that in substance form part of the Group’s net investment in the associate or the joint venture.

Unrealised profits and losses resulting from transactions between the Group and its associate and joint venture are eliminated to the extent of the Group’s interest in the investee, except where unrealised losses provide evidence of an impairment of the asset transferred, in which case they are recognised immediately in profit or loss.

If an investment in an associate becomes an investment in a joint venture or vice versa, retained interest is not remeasured. Instead, the investment continues to be accounted for under the equity method.

In all other cases, when the Group ceases to have significant influence over an associate or joint control over a joint venture, it is accounted for as a disposal of the entire interest in that investee, with a resulting gain or loss being recognised in profit or loss. Any interest retained in that former investee at the date when significant influence or joint control is lost is recognised at fair value and this amount is regarded as the cost on initial recognition of a financial asset (see Note 2(i)).

In the Company’s balance sheet, investments in associates and joint ventures are stated at cost less impairment losses (see Note 2(t)(ii)).

(g) Goodwill

Goodwill represents the excess of the consideration transferred, including the amount of assets transferred (including the acquirer’s previously held equity interest in the acquiree), liabilities incurred or assumed, and the equity securities issued by the acquirer at the date of acquisition, over the fair value of the Group’s share of the identifiable net assets acquired, when the excess is positive, otherwise it’s recognised directly in profit or loss.

Positive goodwill will be stated in the consolidated balance sheet as a separate asset or included within joint ventures and associates at cost less accumulated impairment losses and is subject to impairment testing at least annually. Impairment losses on goodwill are not reversed. Negative goodwill is recognised in profit or loss immediately on acquisition.

(h) Translation of foreign currencies

Foreign currency transactions are, on initial recognition, translated by applying the foreign exchange rates ruling at the transaction dates. Monetary items denominated in foreign currencies are translated at the foreign exchange rates ruling at the reporting date, the resulting exchange differences are recognised in profit or loss. Non-monetary items that are measured in terms of historical cost in a foreign currency are translated using the exchange rates ruling at the transaction dates. Non-monetary items that are measured at fair value in a foreign currency are translated using the foreign exchange rates ruling at the dates the fair value was determined. The exchange differences are recognised in profit or loss, except for the differences arising from the translation of available-for-sale equity investments, which is recognised in other comprehensive income.

The financial statements of the Group’s subsidiaries with a foreign functional currency are translated into HK$ for the preparation of the Group’s consolidated financial statements. The assets and liabilities in these financial statements are translated into HK$ at the foreign exchange rates ruling at the reporting date. The equity items, except for “retained earnings”, are translated to HK$ at the foreign exchange rates at the dates on which such items arose.

Income and expenses in the profit or loss are translated into HK$ at the foreign exchange rates or the rates that approximate the foreign exchange rates at the transaction dates. The resulting exchange differences are presented as “Reserves” (exchange reserve) in the consolidated balance sheet within the shareholder’s equity

Upon disposal of a foreign operation, the cumulative amount of the translation differences recognised in shareholders’ equity which relates to that foreign operation is transferred to profit or loss in the period in which the disposal occurs.

(i) Financial instruments

(i) Initial recognition

The Group classifies its financial instruments into different categories at inception, depending on the purpose for which the assets were acquired or the liabilities were incurred, and on the contractual terms of the financial instruments. The categories are: financial assets or financial liabilities at fair value through profit or loss, loans and receivables, held-to-maturity investments, available-for-sale financial assets and other financial liabilities.

Financial instruments are measured initially at fair value, which normally will be equal to the transaction price plus, in case of a financial asset or financial liability not held at fair value through profit or loss, transaction costs that are directly attributable to the acquisition of the financial asset or issue of the financial liability. Transaction costs on financial assets and financial liabilities at fair value through profit or loss are expensed immediately.

The Group recognises financial assets and financial liabilities on the date it becomes a party to the contractual provisions of the instrument. A regular way purchase or sale of financial assets and financial liabilities at fair value through profit or loss is recognised using trade date accounting. Other financial assets and financial liabilities are recognised using settlement date accounting. From these dates, any gains and losses arising from changes in fair value of the financial assets or financial liabilities at fair value through profit or loss are recorded.

(ii) Categorisation

Financial assets at fair value through profit or loss

This category comprises financial assets held for trading, and those designated at fair value through profit or loss upon initial recognition, but excludes those investments in equity instruments that do not have a quoted market price and whose fair value cannot be reliably measured.

A financial asset is classified as held for trading if it is: (i) acquired principally for the purpose of selling it in the near term; (ii) part of a portfolio of identified financial instruments that are managed together and for which there is evidence of a recent actual pattern of short-term profit-taking; or (iii) a derivative. Derivatives that do not qualify for hedge accounting (Note 2(j)) are accounted for as trading instruments.

Financial instruments are designated at fair value through profit or loss upon initial recognition when:

– the assets are managed, evaluated and reported internally on a fair value basis;

– the designation eliminates or significantly reduces an accounting mismatch in the gain and loss recognition arising from the difference in measurement bases of the financial assets which would otherwise arise;

– the asset contains an embedded derivative that significantly modifies the cash flows that would otherwise be required under the contract; or

– the separation of the embedded derivative(s) from the financial instrument is not prohibited.

Financial assets under this category are carried at fair value. Changes in the fair value are included in profit or loss in the period in which they arise. Upon disposal the difference between the net sale proceeds and the carrying value is included in profit or loss.

Loans and receivables

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market, other than (a) those that the Group intends to sell immediately or in the near term, which will be classified as held for trading; (b) those that the Group, upon initial recognition, designates as at fair value through profit or loss or as available-for-sale; or (c) those where the Group may not recover substantially all of its initial investment, other than because of credit deterioration, which will be classified as available-for-sale.

Loans and receivables mainly comprise loans and advances to customers and other parties, deposits and placements with banks and non-bank financial institutions, financial assets held under resale agreements, investments classified as receivables, and trade and other receivables.

Loans and receivables are carried at amortised cost using the effective interest method, less impairment losses, if any (see Note 2(t)(i)). Where the receivables are interest-free loans made to related parties without any fixed repayment term or the effect of discounting would be immaterial, the receivables are stated at cost less allowance for impairment of doubtful debts.

Held-to-maturity investments

Held-to-maturity investments are non-derivative financial assets with fixed or determinable payments and fixed maturity for which the Group has the positive intention and ability to hold to maturity, other than (a) those that the Group, upon initial recognition, designates as at fair value through profit or loss or as available-for-sale; and (b) those that meet the definition of loans and receivables.

Held-to-maturity investments are carried at amortised cost using the effective interest method less impairment losses, if any (see Note 2(t)(i)).

If, as a result of a change in intention or ability, it is no longer appropriate to classify an investment as held-to-maturity, it shall be reclassified as available-for-sale and remeasured at fair value.

Available-for-sale financial assets

Available-for-sale financial assets are non-derivative financial assets that are designated as availablefor-sale or are not classified in any of the other three categories above. They include financial assets intended to be held for an indefinite period of time, but which may be sold in response to needs for liquidity or changes in the market environment.

Available-for-sale financial assets are carried at fair value. Unrealised gains and losses arising from changes in the fair value are recognised in other comprehensive income and accumulated separately in equity, except for impairment losses and foreign exchange gains and losses on monetary items such as debt securities which are recognised in profit or loss. Dividend income from equity securities and interest income from debt securities calculated using the effective interest method are recognised in profit or loss in accordance with the policies set out in Note 2(w)(vii) and 2(w)(i) respectively.

Investments in equity securities that do not have a quoted market price in an active market and whose fair value cannot be measured reliably, and derivatives that are linked to and must be settled by delivery of such unquoted equity securities are carried at cost less impairment losses, if any (see Note 2(t)(i)).

When the available-for-sale financial assets are sold, gains or losses on disposal include the difference between the net sale proceeds and the carrying value, and the accumulated fair value adjustments which are previously recognised in other comprehensive income shall be reclassified from equity to profit or loss.

Financial liabilities at fair value through profit or loss

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction in the principal (or most advantageous) market at the measurement date under current market conditions (i.e. an exit price) regardless of whether that price is directly observable or estimated using another valuation technique.

A financial liability is classified as held for trading if it is: (i) acquired or incurred principally for the purpose of repurchasing it in the near term; (ii) part of a portfolio of identified financial instruments that are managed together and for which there is evidence of a recent actual pattern of short-term profit-taking; or (iii) a derivative (except for a derivative that is a financial guarantee contract or a designated and effective hedging instrument).

Financial liabilities are designated at fair value through the profit or loss upon initial recognition when: (i) the financial liabilities or are managed, evaluated and reported internally on a fair value basis; (ii) the designation eliminates or significantly reduces an accounting mismatch in the gain and loss recognition arising from the difference in measurement bases of the financial liabilities; or (iii) a contract contains one or more embedded derivatives, i.e. an entire hybrid (combined) contract, unless: (i) the embedded derivative does not significantly modify the cash flows that otherwise would be required by the hybrid (combined) contract; or (ii) it is clear with little or no analysis when a similar hybrid (combined) instrument is first considered that separation of the embedded derivative is prohibited.

Other financial liabilities

Financial liabilities, other than trading liabilities and those designated at fair value through profit or loss, are measured at amortised cost using the effective interest method.

Other financial liabilities mainly comprise borrowing from central banks, deposits from banks and non-bank financial institutions, placements from banks and non-bank financial institutions, trade and other payables, financial assets sold under repurchase agreements, deposits from customers, banks and other loans, and debt instruments issued.

(iii) Fair value measurement principles

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction in the principal (or most advantageous) market at the measurement date under current market conditions (i.e. an exit price) regardless of whether that price is directly observable or estimated using another valuation technique.

If there is no publicly available latest traded price nor a quoted market price on a recognised stock exchange or a price from a broker/dealer for non-exchange-traded financial instruments, or if the market for it is not active, the fair value of the instrument is estimated using valuation techniques that provide a reliable estimate of prices which could be obtained in actual market transactions.

Where discounted cash flow techniques are used, estimated future cash flows are based on management’s best estimates and the discount rate is based on the relevant government yield curve as at the balance sheet date plus an adequate constant credit spread. Where other pricing models are used, inputs are based on market data at the balance sheet date.

(iv) Derecognition

A financial asset is derecognised when the contractual rights to receive the cash flows from the financial asset expire, or where the financial asset together with substantially all the risks and rewards of ownership, have been transferred.

The Group derecognises a financial asset, if the part being considered for derecognition meets one of the following conditions: (a) the contractual rights to receive the cash flows from the financial asset expire; or (b) the contractual rights to receive the cash flows of the financial asset have been transferred, and the Group transfers substantially all the risks and rewards of ownership of the financial asset; or (c) the Group retains the contractual rights to receive the cash flows of the financial asset, but assumes a contractual obligation to pay the cash flows to the eventual recipient in an agreement that meets all the conditions of derecognition of transfer of cash flows and transfers substantially all the risks and rewards of ownership of the financial asset.

Where a transfer of a financial asset in its entirety meets the criteria for derecognition, the difference between the two amounts below is recognised in profit or loss:

– the carrying amount of the financial asset transferred;

– the sum of the consideration received from the transfer and any cumulative gain or loss that has been recognised directly in equity.

If the Group neither transfers nor retains substantially all the risks and rewards of ownership of the financial asset, but retains control, the Group continues to recognise the financial asset to the extent of its continuing involvement in the financial asset. If the Group has not retained control, it derecognises the financial asset and recognises separately as assets or liabilities any rights and obligations created or retained in the transfer.

As part of its operational activities, the Group securitises financial assets, generally through the sale of these assets to structured entities which issue securities to investors. Further details on prerequisites for derecognition of financial assets are set out above. When the securitisation of financial assets that do qualify for derecognition, the relevant financial assets are derecognised in their entirety and a new financial asset or liabilities is recognised regarding the interest in unconsolidated securitisation vehicles that the Group receives as part of the transfer. When the securitisation of financial assets that do not qualify for derecognition, the relevant financial assets are not derecognised, and the consideration paid by third parties are recorded as a financial liability; when the securitisation of financial assets that partially qualify for derecognition, the book value of the transferred asset should be recognised between the derecognised portion and the retained portion based on their respective relative fair values, and the difference between the book value of the derecognised portion and the total consideration paid for the derecognised portion shall be recorded in profit or loss.

The derecognition of financial assets sold on condition of repurchase is determined by the economic substance of the transaction. If a financial asset is sold under an agreement to repurchase the same or substantially the same asset at a fixed price or at the sale price plus a reasonable return, the Group will not derecognise the asset. If a financial asset is sold together with an option to repurchase the financial asset at its fair value at the time of repurchase (in case of transferor sells such financial asset), the Group will derecognise the financial asset.

The financial liability is derecognised only when: (a) the underlying present obligation specified in the contracts is discharged/cancelled, or (b) an agreement between the Group and an existing lender to exchange the original financial liability with a new financial liability with substantially different terms, or a substantial modification of the terms of an existing financial liability is accounted for as an extinguishment of the original financial liability and recognition of a new financial liability. The difference between the carrying amount of the financial liability derecognised and the consideration paid is recognised in profit or loss.

(v) Offsetting

Financial assets and financial liabilities are offset and the net amount is reported in the balance sheet where there is a legally enforceable right to offset the recognised amounts and there is an intention to settle on a net basis, or realise the asset and settle the liability simultaneously.

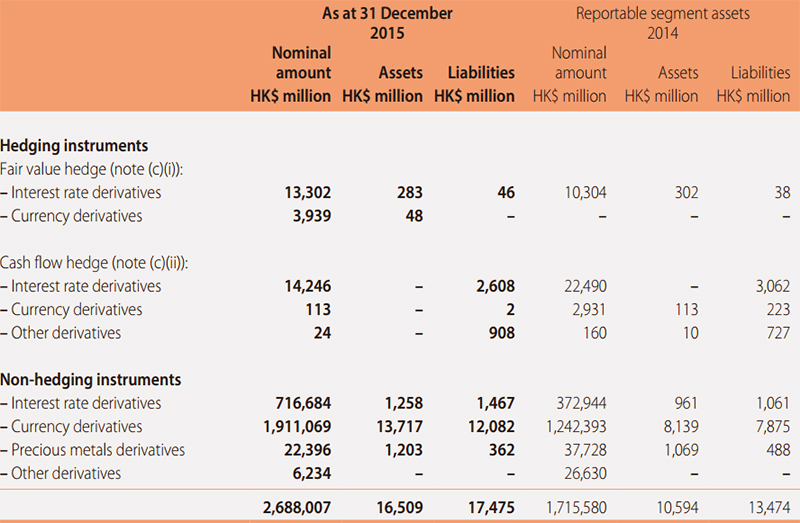

(vi) Derivatives

The Group uses derivatives to hedge its exposure on risks. The Group adopts hedge accounting in accordance with Note 2(j) for derivatives designated as hedging instruments if the hedge is effective. Other derivatives are accounted for as trading financial assets or financial liabilities. Derivatives are recognised at fair value upon initial recognition. The positive fair value is recognised as assets while the negative fair value is recognised as liabilities. The gain or loss on re-measurement to fair value is recognised immediately in profit or loss.

(vii) Embedded derivatives

An embedded derivative is a component of a hybrid (combined) instrument that includes both the derivative and a host contract with the effect that some of the cash flows of the combined instrument vary in a way similar to a stand-alone derivative. The embedded derivatives are separated from the host contract and accounted for as a derivative when (a) the economic characteristics and risks of the embedded derivative are not closely related to the host contract; and (b) the hybrid (combined) instrument is not measured at fair value with changes in fair value recognised in profit or loss.

When the embedded derivative is separated, the host contract is accounted for in accordance with Note 2(i)(ii) above.

(j) Hedging

Hedge accounting recognises the offsetting effects on profit or loss of changes in the fair values of the hedging instrument and the hedged item. The Group assesses and documents whether the financial instruments that are used in hedging transactions are highly effective in offsetting changes in fair values or cash flows of hedged items attributable to the hedged risks both at hedge inception and on an ongoing basis. The Group discontinues prospectively hedge accounting when (a) the hedging instrument expires or is sold, terminated or exercised; (b) the hedge no longer meets the criteria for hedge accounting; or (c) the Group revokes the designation.

(i) Fair value hedge

A fair value hedge seeks to offset risks of changes in the fair value of recognised asset or liability that will give rise to a gain or loss being recognised in profit or loss. The hedging instrument is measured at fair value, with fair value changes recognised in profit or loss. The carrying amount of the hedged item is adjusted by the amount of the changes in fair value of the hedging instrument attributable to the risk being hedged. This adjustment is recognised in profit or loss to offset the effect of the gain or loss on the hedging instrument.

When a hedging instrument expires or is sold, terminated or exercised, the hedge no longer meets the criteria for hedge accounting, or the Group revokes designation of the hedge relationship, any adjustment up to that point, to a hedged item for which the effective interest method is used, is amortised to profit or loss as part of the recalculated effective interest rate of the item over its remaining life.

(ii) Cash flow hedge

Where a derivative financial instrument is designated as a hedge of the variability in cash flows of a recognised asset or liability, or a highly probable forecast transaction, or the foreign currency risk of a committed future transaction, the effective part of any gain or loss on remeasurement of the derivative financial instrument to fair value is recognised in other comprehensive income and accumulated separately in equity in the hedging reserve. The ineffective portion of any gain or loss is recognised immediately in profit or loss.

If the hedge of a forecast transaction subsequently results in the recognition of a non-financial asset or non-financial liability, the associated gain or loss is reclassified from equity to be included in the initial cost or other carrying amount of the non-financial asset or liability

If a hedge of a forecast transaction subsequently results in the recognition of a financial asset or a financial liability, the associated gain or loss is reclassified from equity to the profit or loss in the same period or periods during which the asset acquired or liability assumed affects the profit or loss (such as when interest income or expense is recognised).

For cash flow hedges, other than those covered by the preceding two policy statements, the associated gain or loss is reclassified from equity to profit or loss in the same period or periods during which the hedged forecast transaction affects profit or loss.

When a hedging instrument expires or is sold, terminated or exercised, or the Group revokes designation of the hedge relationship but the hedged forecast transaction is still expected to occur, the cumulative gain or loss at that point remains in equity until the transaction occurs and is recognised in accordance with the above policy. If the hedged transaction is no longer expected to take place, the cumulative unrealised gain or loss is reclassified from equity to profit or loss immediately.

(iii) Hedge effectiveness testing

In order to qualify for hedge accounting, the Group carries out prospective effectiveness testing to demonstrate that it expects the hedge to be highly effective at the inception of the hedge and throughout its life. Actual effectiveness (retrospective effectiveness) is also demonstrated on an ongoing basis.

The documentation of each hedging relationship sets out how the effectiveness of the hedge is assessed. The method which the Group adopts for assessing hedge effectiveness will depend on its risk management strategy.

For fair value hedge relationships, the Group utilises the cumulative dollar offset method or regression analysis as effectiveness testing methodologies. For cash flow hedge relationships, the Group utilises the change in variable cash flow method or the cumulative dollar offset method using the hypothetical derivative approach.

For prospective effectiveness, the hedging instrument must be expected to be highly effective in achieving offsetting changes in fair value or cash flows attributable to the hedged risk during the period for which the hedge is designated. For actual effectiveness, the changes in fair value or cash flows must offset each other in the range of 80 per cent to 125 per cent for the hedge to be deemed effective.

(k) Financial assets held/sold under resale/repurchase agreements

Financial assets held under resale agreements are transactions that the Group acquires financial assets which will be resold at a predetermined price in the future date under resale agreements. Financial assets sold under repurchase agreements are transactions that the Group sells financial assets which will be repurchased at a predetermined price in the future date under repurchase agreements.

The cash advanced or received is recognised as amounts held under the resale and repurchase agreements in the balance sheet. Assets held under resale agreements are recorded in memorandum accounts as off-balance sheet items. Assets sold under repurchase agreements continue to be recognised in the balance sheet.

The difference between the sale and repurchase consideration, and that between the purchase and resale consideration, are amortised over the period of the respective transaction using the effective interest method and are included in interest income and interest expense respectively.

(l) Investment properties

Investment properties are interests in land and/or buildings which are held to earn rentals or for capital appreciation or both. These include land held for a currently undetermined future use. Land held under operating leases is classified and accounted for as investment property when the rest of the definition of investment property is met.

Investment properties are stated in the balance sheet at fair values which are reviewed annually. Any gain or loss arising from a change in fair value or from the retirement or disposal of an investment property is recognised in profit or loss.

(m) Property, plant and equipment

Property, plant and equipment are carried at cost less accumulated depreciation and accumulated impairment losses (Note 2(t)(ii)).

Assets in the course of construction for production, rental or administrative purposes are carried at cost, less any impairment losses. Cost includes the cost of materials, direct labour, the initial estimate, where relevant, of the costs of dismantling and removing the items and restoring the site on which they are located, and an appropriate proportion of overheads.

Construction-in-progress represents property, plant and equipment under construction and is transferred to fixed assets when ready for its intended use.

No depreciation is provided in respect of construction in progress. Upon completion and commissioning for operation, depreciation will be provided at the appropriate rate specified below.

Property, plant and equipment are depreciated at rates sufficient to write off their cost, less impairment losses, if any, to their estimated residual values, over their estimated useful lives on a straight line basis as follows:

– Plant and buildings 5–70 years – Machinery and equipment 3–26 years – Office and other equipment, vehicles and vessels and others 3–10 years Freehold land within the category of plant and buildings are not depreciated.

Assets’ useful lives and residual values are reviewed, and adjusted if appropriate, at each balance sheet date.

An asset’s carrying amount is written down immediately to its recoverable amount if the asset’s carrying amount is greater than its estimated recoverable amount.

The recoverable amount of an asset is the greater of its fair value less costs of disposal and value in use.

Gains and losses on disposals are determined by comparing the proceeds with the carrying amount and are recognised in profit or loss.

(n) Land use rights

Land use rights are stated at cost less accumulated amortisation and accumulated impairment losses (if any). Land use rights are amortised on a straight-line basis over the respective periods of grant, usually within 10 to 50 years.

Impairment losses on land use rights are accounted for in accordance with the accounting policies as set out in Note 2(t)(ii).

(o) Intangible assets (other than goodwill)

Intangible assets acquired by the Group are stated at cost less accumulated amortisation (where the estimated useful life is finite) and impairment losses (see Note 2(t)(ii)).

Amortisation of intangible assets with finite useful lives is charged to profit or loss over the assets’ estimated useful lives. The following intangible assets are amortised from the date they are available for use as follows:

– Roads and tunnels operating rights Over the estimated useful lives of 30 years – Mining assets Over the estimated useful lives of the mines in

accordance with the production plan of the entities

concerned and the proven probable reserves of the

mines using the unit-of-production method.Both the period and method of amortisation are reviewed annually.

Intangible assets are not amortised while their useful lives are assessed to be indefinite. Any conclusion that the useful life of an intangible asset is indefinite is reviewed annually to determine whether events and circumstances continue to support the indefinite useful life assessment for that asset. If they do not, the change in the useful life assessment from indefinite to finite is accounted for prospectively from the date of change and in accordance with the policy for amortisation of intangible assets with finite lives as set out above.

(p) Inventories

(i) Manufacturing, resources and energy segments

Inventories of the manufacturing, and resources and energy segments are carried at the lower of cost and net realisable value.

Cost is calculated using the first-in first-out, specific identification or weighted average cost formula as appropriate, and comprises all costs of purchase, costs of conversion and other costs incurred in bringing the inventories to their present location and condition.

Net realisable value is the estimated selling price in the ordinary course of business less the estimated costs of completion and the estimated costs necessary to make the sale.

When inventories are sold, the carrying amount of those inventories is recognised as an expense in the period in which the related revenue is recognised. The amount of any write-down of inventories to net realisable value and all losses of inventories are recognised as an expense in the period the write-down or loss occurs. The amount of any reversal of any write-down of inventories is recognised in profit or loss in the period in which the reversal occurs.

(ii) Real estate segment

Inventories in respect of property development activities under the real estate segment are carried at the lower of cost and net realisable value. Cost and net realisable values are determined as follows:

– Property under development

The cost of properties under development comprises specifically identified cost, including the acquisition cost of land, aggregate cost of development, materials and supplies, wages and other direct expenses, an appropriate proportion of overheads and borrowing costs capitalised (see Note 2(bb)). Net realisable value represents the estimated selling price less estimated costs of completion and costs to be incurred in selling the property.。

– Completed property held for sale

In the case of completed properties developed by the Group, cost is determined by apportionment of the total development costs for that development project, attributable to the unsold properties. Net realisable value represents the estimated selling price less costs to be incurred in selling the property.

The cost of completed properties held for sale comprises all costs of purchase, costs of conversion and other costs incurred in bringing the inventories to their present location and condition.

(q) Construction contracts

Construction contracts are contracts specifically negotiated with a customer for the construction of an asset or a group of assets, where the customer is able to specify the major structural elements of the design. The accounting policy for contract revenue is set out in Note 2(w)(v). When the outcome of a construction contract can be estimated reliably, contract costs are recognised as an expense by reference to the stage of completion of the contract at the balance sheet date. When it is probable that total contract costs will exceed total contract revenue, the expected loss is recognised as an expense immediately. When the outcome of a construction contract cannot be estimated reliably, contract costs are recognised as an expense in the period in which they are incurred.

Construction contracts in progress at the balance sheet date are recorded at the net amount of costs incurred plus recognised profit less recognised losses and progress billings, and are presented in the balance sheet as “amount due from customers for contract work” or “amount due to customers for contract work”.

(r) Operating leases

Leases which do not transfer substantially all the risks and rewards of ownership to the lessee are classified as operating leases.

Where the Group leases out assets under operating leases, the assets are included in the balance sheet according to their nature and, where applicable, are depreciated in accordance with the Group’s depreciation policies, as set out in Note 2(m) except where the asset is classified as an investment property. Impairment losses are accounted for in accordance with the accounting policy as set out in Note 2(t)(ii). Revenue arising from operating leases is recognised in accordance with the Group’s revenue recognition policies, as set out in Note 2(w)(vi).

Where the Group has the use of assets held under operating leases, payments made under the leases are charged to profit or loss in equal instalments over the accounting periods covered by the lease term, except where an alternative basis is more representative of the pattern of benefits to be derived from the leased asset. Lease incentives received are recognised in profit or loss as an integral part of the aggregate net lease payments made. Contingent rentals are charged to profit or loss in the accounting period in which they are incurred.

The cost of acquiring land held under an operating lease is amortised on a straight-line basis over the period of the lease term except where the property is classified as an investment property (see Note 2(l)).

(s) Repossessed assets

In the recovery of impaired loans and advances, the Group may take possession of assets held as collateral through court proceedings or voluntary delivery of possession by the borrowers. Where it is intended to achieve an orderly realisation of the impaired assets and the Group is no longer seeking repayment from the borrower, repossessed assets are reported in “other assets”.

When the Group seizes assets to compensate for the losses of loans and advances and interest receivables, the repossessed assets are initially recognised at fair value, plus any taxes paid for the seizure of the assets, litigation fees and other expenses incurred for collecting the repossessed assets are included in the carrying value of repossessed assets. Repossessed assets are recognised at the carrying value, net of allowances for impairment losses.

Impairment losses on initial recognition and on subsequent remeasurement are recognised in profit or loss.

(t) Impairment of assets

(i) Financial assets

The carrying amounts of the Group’s financial assets other than those measured at fair value through profit and loss are reviewed at balance sheet date to determine whether there is objective evidence of impairment. Objective evidence that financial assets are impaired includes but not limited to one or more of the following loss events that occurred after the initial recognition of the asset and has an impact on the future cash flows on the assets that can be estimated reliably:

– significant financial difficulty of the issuer or borrower;

– a breach of contract, such as a default or delinquency in interest or principal payments;

– the Group, for economic or legal reasons relating to the borrower’s financial difficulty, granting to the borrower a concession that the Group would not otherwise consider;

– it becoming probable that the borrower will enter bankruptcy or other financial reorganisation;

– disappearance of an active market for financial assets because of financial difficulties;

– observable data indicating that there is a measurable decrease in the estimated future cash flows from a group of financial assets since the initial recognition of those assets, although the decrease cannot yet be identified with the individual financial assets in the Group, including: adverse changes in the payment status of borrowers in the Group, an increase in the unemployment rate in the geographical area of the borrowers, a decrease in property prices for mortgages in the relevant area, or adverse changes in industry conditions that affect the borrowers in the Group;

– significant changes in the technological, market, economic or legal environment that have an adverse effect on the issuer;

– a significant or prolonged decline in the fair value of an investment in an equity instrument below its cost; and

– other objective evidence indicating there is an impairment of a financial asset.

If any such evidence exists, the carrying amount is reduced to the estimated recoverable amount by means of a charge to profit or loss.

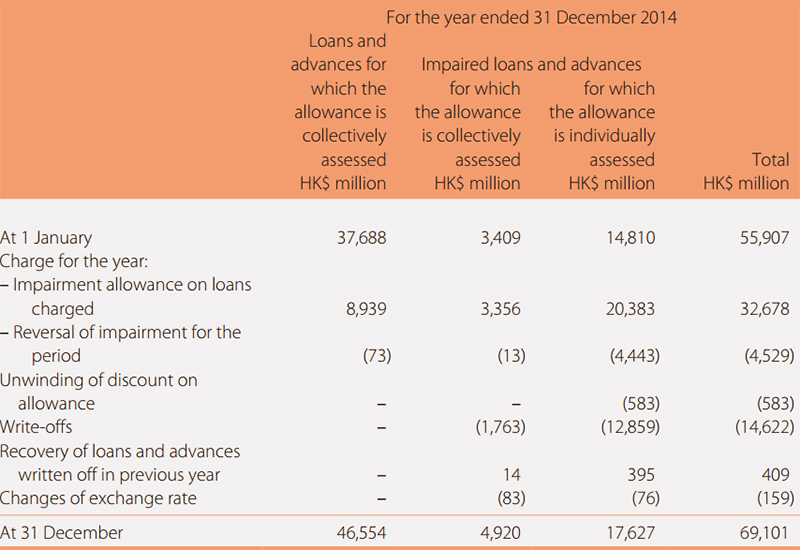

Impairment losses are written off against the corresponding assets directly, except for impairment losses recognised in respect of loans and receivables and held-to-maturity investments, which are measured at amortised cost, whose recovery is considered doubtful but not remote. In this case, the impairment losses are recorded using an allowance account. When the Group is satisfied that recovery is remote after all the necessary legal or other proceedings are completed, the amount considered irrecoverable is written off against loans and receivables or held-to-maturity investments directly and any amounts held in the allowance account relating to that borrower/investment are reversed. Subsequent recoveries of amounts previously charged to the allowance account are reversed against the allowance account. Other changes in the allowance account and subsequent recoveries of amounts previously written off directly are recognised in profit or loss.

Loans and receivables

Impairment losses on loans and receivables are measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows discounted at the asset’s original effective interest rate (i.e. the effective interest rate computed at initial recognition of these assets). Receivables with a short duration are not discounted if the effect of discounting is immaterial.

The total allowance for credit losses consists of two components: individual impairment allowances, and collective impairment allowances.

The Group first assesses whether objective evidence of impairment exists individually for financial assets that are individually significant, and collectively for financial assets that are not individually significant. If the Group determines that no objective evidence of impairment exists for an individually assessed financial asset, whether significant or not, it includes the asset in a group of financial assets with similar credit risk characteristics and collectively assesses them for impairment. Assets that are individually assessed for impairment and for which an impairment loss is or continues to be recognised are not included in a collective assessment of impairment.

The individual impairment allowance is based upon management’s best estimate of the present value of the cash flows which are expected to be received, discounted at the original effective interest rate. In estimating these cash flows, management makes judgements about the borrower’s financial situation and the net realisable value of any underlying collateral or guarantees in favour of the Group. Each impaired asset is assessed on its own merits.

In assessing the need for collective loan loss allowances, management uses statistical modelling and considers historical trends of factors such as credit quality, portfolio size, concentrations, and economic factors. In order to estimate the required allowance, the Group makes assumptions both to define the way the Group models inherent losses and to determine the required input parameters, based on historical experience and current economic conditions.

The accuracy of the impairment allowances the Group makes depends on how well the Group can estimate future cash flows for individually assessed impairment allowances and the model assumptions and parameters used in determining collective impairment allowances. While this necessarily involves judgement, the Group believes that the impairment allowances on loans and advances to customers are reasonable and supportable.

Any subsequent changes to the amounts and timing of the expected future cash flows compared to the prior estimates that can be linked objectively to an event occurring after the write-down, will result in a change in the impairment allowances on loans and receivables and be charged or credited to the income statement. A reversal of impairment losses is limited to the loans and receivables’ carrying amount that would have been determined had no impairment loss been recognised in prior years.

When there is no reasonable prospect of recovery, the loan and the related interest receivables are written off.

Loans and receivables with renegotiated terms are loans that have been restructured due to deterioration in the borrower’s financial position and where the Group has made concessions that it would not otherwise consider. Renegotiated loans and receivables are subject to ongoing monitoring to determine whether they remain impaired or past due.

Held-to-maturity investments

Impairment on held-to-maturity investments is considered at both an individual and collective level. The individual impairment allowance is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows, discounted at the asset’s original effective interest rate, where the effect of discounting is material.

All significant assets found not to be individually impaired are then collectively assessed for any impairment that has been incurred but not yet identified. Assets that are not individually significant are then collectively assessed for impairment by grouping together financial assets with similar risk characteristics.

If in a subsequent period the amount of an impairment loss decreases and the decrease can be linked objectively to an event occurring after the impairment loss was recognised, the impairment loss is reversed through the income statement. A reversal of impairment losses shall not result in the asset’s carrying amount exceeding that which would have been determined had no impairment loss been recognised in prior years.

Available-for-sale financial assets

When there is objective evidence that an available-for-sale financial asset is impaired, the cumulative loss that had been recognised in the fair value reserve is reclassified to profit or loss. The amount of the cumulative loss that is recognised in profit or loss is the difference between the acquisition cost (net of any principal repayment and amortisation) and current fair value, less any impairment loss on that asset previously recognised in profit or loss.

For unquoted available-for-sale equity securities that are carried at cost, the impairment loss is measured as the difference between the carrying amount of the equity securities and the estimated future cash flows, discounted at the current market rate of return for a similar financial asset where the effect of discounting is material. Such impairment losses are not reversed.

Impairment losses recognised in profit or loss in respect of available-for-sale equity securities are not reversed through profit or loss. Any subsequent increase in the fair value of such assets is recognised in other comprehensive income.

Impairment losses in respect of available-for-sale debt securities are reversed if the subsequent increase in fair value can be objectively related to an event occurring after the impairment loss was recognised. Reversals of impairment losses in such circumstances are recognised in profit or loss.

(ii) Non-financial assets

Internal and external sources of information are reviewed at balance sheet date to identify indications that the following assets may be impaired or, except in the case of goodwill, an impairment loss previously recognised no longer exists or may have decreased:

– property, plant and equipment (other than properties carried at revalued amounts);

– land use rights;

– investments in subsidiaries, associates and joint ventures;

– goodwill; and

– intangible assets.

If any such indication exists, the asset’s recoverable amount is estimated. In addition, for goodwill and intangible assets that are not yet available for use and intangible assets that have indefinite useful lives, the recoverable amount is estimated annually whether or not there is any indication of impairment.

Calculation of recoverable amount

The recoverable amount of an asset is the greater of its fair value less costs of disposal and value in use. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of time value of money and the risks specific to the asset. Where an asset does not generate cash inflows largely independent of those from other assets, the recoverable amount is determined for the smallest group of assets that generates cash inflows independently (i.e. a cash-generating unit).

Recognition of impairment losses

An impairment loss is recognised in profit or loss whenever the carrying amount of an asset, or the cash-generating unit to which it belongs, exceeds its recoverable amount. Impairment losses recognised in respect of cash-generating units are allocated first to reduce the carrying amount of any goodwill allocated to the cash-generating unit (or group of units) and then, to reduce the carrying amount of the other assets in the unit (or group of units) on a pro rata basis, except that the carrying value of an asset will not be reduced below its individual fair value less costs of disposal (if measurable) or value in use (if determinable).

Reversals of impairment losses

If, in a subsequent period, the amount of impairment loss of the non-financial asset except for goodwill decreases and the decrease can be linked objectively to an event occurring after the impairment was recognised, the previously recognised impairment loss is reversed through the profit or loss. A reversal of impairment loss is limited to the asset’s carrying amount that would have been determined had no impairment loss been recognised in prior periods.

An impairment loss in respect of goodwill is not reversible.

(u) Employee benefits

(i) Short-term employee benefits

During the accounting period when an employee has rendered service to the Group, the Group recognises the undiscounted amount of short-term employee benefits as a liability and as an expense, unless another HKFRS requires or permits the inclusion of the benefits in the cost of an asset. Short-term employee benefits include wages, bonuses and social security contributions such as medical insurance, work-related injury insurance and maternity insurance, as well as housing provident funds, which are all calculated based on the regulated benchmark and ratio. Where the payment of liability is expected not to be settled wholly before twelve months after the end of the annual reporting period in which the employees render the related services, and the effect would be material, these liabilities are stated at their present values in the balance sheet.

(ii) Defined contribution retirement schemes

Employees of the Group’s subsidiaries in Hong Kong are offered the option to enroll in one of the Mandatory Provident Fund (“MPF”) Master Trust Schemes under the CITIC Group MPF Scheme. The MPF Master Trust Schemes are defined contribution schemes and are administered in accordance with the terms and provisions of the respective trust deeds and are subject to the Mandatory Provident Fund Schemes Ordinance.

Employees of the Group’s PRC subsidiaries are required to participate in defined contribution retirement schemes and make contributions according to the respective regulations. Employees of the Group’s PRC subsidiaries are also eligible to participate in the enterprise annuity plan established by the Group according to the relevant requirements.

Employees of the Group’s overseas subsidiaries are required to make contributions subjected to the relevant regulations in the countries/jurisdiction in which the overseas subsidiaries operate.

The contributions are charged to profit and loss for the current period on an accrual basis.

(v) Financial guarantees issued, provisions and contingent liabilities

(i) Financial guarantees issued

Financial guarantees are contracts that require the issuer (i.e. the guarantor) to make specified payments to reimburse the beneficiary of the guarantee (the “holder”) for a loss the holder incurs because a specified debtor fails to make payment when due in accordance with the terms of a debt instrument.

Where the Group issues a financial guarantee, the fair value of the guarantee is initially recognised as deferred income within “other liabilities”. The fair value of financial guarantees issued at the time of issuance is determined by reference to fees charged in an arm’s length transaction for similar services, when such information is obtainable, or is otherwise estimated by reference to interest rate differentials, by comparing the actual rates charged by lenders when the guarantee is made available with the estimated rates that lenders would have charged, had the guarantees not been available, where reliable estimates of such information can be made. Where consideration is received or receivable for the issuance of the guarantee, the consideration is recognised in accordance with the Group’s policies applicable to that category of asset. Where no such consideration is received or receivable, an immediate expense is recognised in profit or loss on initial recognition of any deferred income.

The amount of the guarantee initially recognised as deferred income is amortised in profit or loss over the term of the guarantee as income from financial guarantees issued. In addition, provisions are recognised in accordance with Note 2(v)(iii) if and when: (1) it becomes probable that the holder of the guarantee will call upon the Group under the guarantee; and (2) the amount of that claim on the Group is expected to exceed the amount currently carried in other liabilities in respect of that guarantee i.e. the amount initially recognised, less accumulated amortisation.

(ii) Contingent liabilities assumed in business combinations

Contingent liabilities assumed in a business combination which are present obligations at the date of acquisition are initially recognised at fair value, provided the fair value can be reliably measured. After their initial recognition at fair value, such contingent liabilities are recognised at the higher of the amount initially recognised, less accumulated amortisation where appropriate, and the amount that would be determined in accordance with Note 2(v)(iii). Contingent liabilities assumed in a business combination that cannot be reliably fair valued or were not present obligations at the date of acquisition are disclosed in accordance with Note 2(v)(iii).

(iii) Other provisions and contingent liabilities

Provisions are recognised for other liabilities of uncertain timing or amount when the Group has a legal or constructive obligation arising as a result of a past event, it is probable that an outflow of economic benefits will be required to settle the obligation and a reliable estimate can be made. A provision is initially measured at the best estimate of the expenditure required to settle the related present obligation. Factors pertaining to a contingency such as the risks, uncertainties and time value of money are taken into account as a whole in reaching the best estimate. Where the time value of money is material, provisions are stated at the present value of the expenditure expected to settle the obligation.

Where it is not probable that an outflow of economic benefits will be required, or the amount cannot be estimated reliably, the obligation is disclosed as a contingent liability, unless the probability of outflow of economic benefits is remote. Possible obligations, whose existence will only be confirmed by the occurrence or non-occurrence of one or more future events are also disclosed as contingent liabilities unless the probability of outflow of economic benefits is remote.

(w) Revenue recognition

Revenue is measured at the fair value of the consideration received or receivable. Provided it is probable that the economic benefits will flow to the Group and the revenue and costs, if applicable, can be measured reliably, revenue is recognised in profit or loss as follows:

(i) Interest income

Interest income arising from the use of entity assets by others is recognised in profit or loss based on the duration and the effective interest rate. Interest income includes the amortisation of any discount or premium or other differences between the initial carrying amount of an interest bearing instrument and its amount at maturity calculated on an effective interest rate basis.

The effective interest method is a method of calculating the amortised cost of financial assets and liabilities and of allocating the interest income and interest expense over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash payments or receipts through the expected life of the financial instrument or, when appropriate, a shorter period to the net carrying amount of the financial instrument. When calculating the effective interest rate, the Group estimates cash flows considering all contractual terms of the financial instrument (for example, call and similar options) but does not consider future credit losses. The calculation includes all fees and interests paid or received between parties to the contract that are an integral part of the effective interest rate, transaction costs and all other premiums or discounts.

Interest on the impaired financial assets is recognised using the rate of interest used to discount future cash flows (“unwinding of discount”) for the purpose of measuring the related impairment loss.

(ii) Fee and commission income

Fee and commission income is recognised when the corresponding service is provided.

Origination or commitment fees received/paid by the Group which result in the creation or acquisition of a financial asset are deferred and recognised as an adjustment to the effective interest rate. When a loan commitment is not expected to result in the draw-down of a loan, loan commitment fees are recognised.

(iii) Sales of goods and services

Revenue is recognised when goods are delivered at the customers’ premises which is taken to be the point in time when the customer has accepted the goods and the related risks and rewards of ownership. Revenue excludes value added tax or other sales taxes and is after deduction of any trade discounts.

Service fee income is recognised when the services are rendered.

(iv) Sales of properties

Revenue from sales of properties is only recognised when the significant risks and rewards of ownership have been transferred to the buyer. The Group considers that the significant risks and rewards of ownership are transferred when the buildings contracted for sale are completed and the relevant permits essential for the delivery of the properties have been issued by the authorities.

(v) Contract revenue

When the outcome of a construction contract can be estimated reliably, revenue from a fixed price contract is recognised using the percentage of completion method.

The Group measured the stage of completion by reference to the percentage of contract costs incurred to date to estimated total contract costs for the contract.

When the outcome of a construction contract cannot be estimated reliably, revenue is recognised only to the extent of contract costs incurred that it is probable will be recoverable.

(vi) Rental income from operating leases

Rental income receivable under operating leases is recognised in profit or loss in equal instalments over the periods covered by the lease term, except where an alternative basis is more representative of the pattern of benefits to be derived from the use of the leased asset. Lease incentives granted are recognised in profit or loss as an integral part of the aggregate net lease payments receivable. Contingent rentals are recognised as income in the accounting period in which they are earned.

(vii) Dividend income

Dividend income from unlisted investments is recognised when the shareholder’s right to receive payment is established. Dividend income from listed investments is recognised when the share price of the investment goes ex-dividend.

(viii) Government grants